Kolmogorov continuity theorem

In stochastic analysis, the Kolmogorov continuity thoerem guarantees the Hölder continuity of a stochastic process using a distance inequality.

Kolmogorov continuity theorem

Let

be some metric space, and

be a stochastic process. Suppose there exist positive constants

such that

for all

, then there exists a modification

of

that is a continuous process, i.e., a process

such that

- For every time

,

.

Furthermore, the paths of

-Hölder continuous for every

.

![\mathbb E[d(X_t,X_s)^\alpha] \le K|t-s|^{1+\beta}](https://s0.wp.com/latex.php?latex=%5Cmathbb+E%5Bd%28X_t%2CX_s%29%5E%5Calpha%5D+%5Cle+K%7Ct-s%7C%5E%7B1%2B%5Cbeta%7D&bg=ffffff&fg=000&s=0&c=20201002)

This result can be employed to obtain the Hölder continuity of a large variety of stochastic processes, and we begin with the simplest example, the standard Brownian motion.

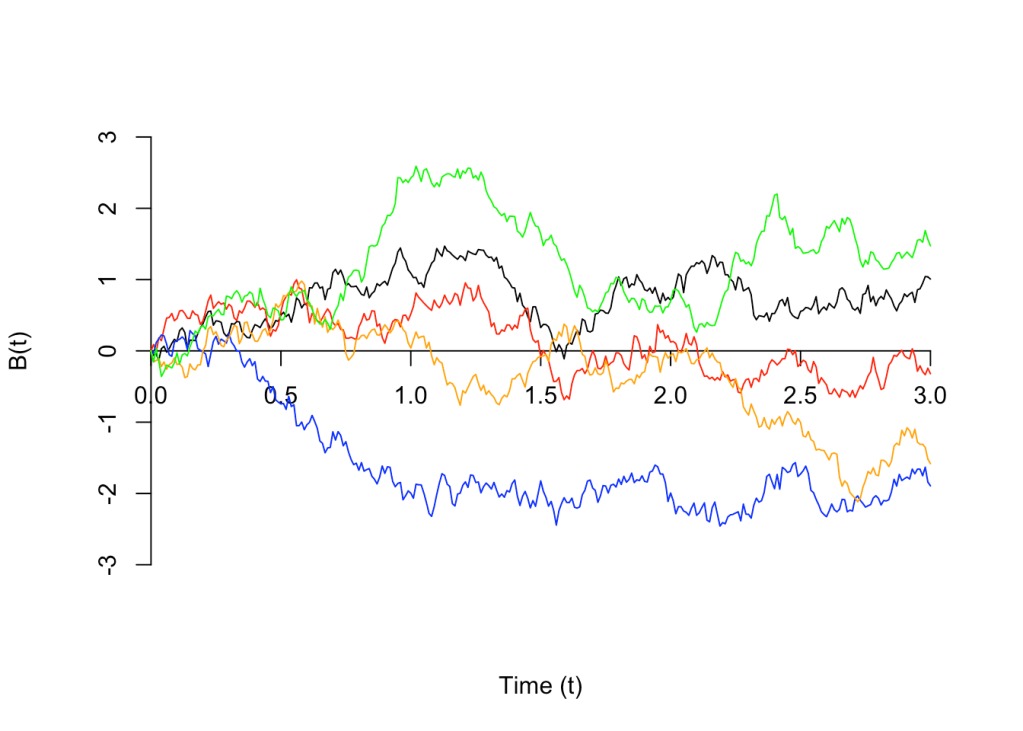

Samples of the trajectories of the Brownian motion.

The Brownian motion

for any

![\displaystyle\mathbb E \bigg[\sup_{s,t\ge 0} \frac{|B_t - B_s|^2}{t-s} \bigg]\le 1](https://s0.wp.com/latex.php?latex=%5Cdisplaystyle%5Cmathbb+E+%5Cbigg%5B%5Csup_%7Bs%2Ct%5Cge+0%7D+%5Cfrac%7B%7CB_t+-+B_s%7C%5E2%7D%7Bt-s%7D+%5Cbigg%5D%5Cle+1&bg=ffffff&fg=000&s=0&c=20201002)

but this is absolutely incorrect because it changes the order of the expectation and the supremum.

The correct way to prove the continuity is to observe that for any positive integer

for any

Finally, since

Karhunen-Loève expansion

The Brownian motion has an alternative expression, the Karhunen-Loève expansion. The Brownian motion

where

Consider the stochastic process

given by

,

where

are a set of functions satisfying

for any

and

, then for any positive integer

As a consequence,

is

.

Proof By direct calculation, we have

Here, the odd power of

Here,

To prove the inequality, divide the summation in the LHS into two parts.

and thus we obtain the desired result.

Summary

We employ the Kolmogorov continuity theorem to obtain the Hölder continuity of the Brownian motion and a general class of stochastic processes. Readers can also refer to Lemma 3.2 of my recent paper for an interesting application of the result.

留下评论